DePIN Data Markets: When the Buyer Already Exists

Most DePIN networks share the same bet: deploy nodes first, find customers later.

It's a reasonable bet. Build enough supply-side coverage and demand will come. Helium spent years on this before landing carrier deals with T-Mobile. DIMO is aggregating vehicle data with the expectation that insurers and OEMs will eventually pay for it. Hivemapper is mapping roads, banking on the idea that mapping customers will materialize at scale.

Sometimes the bet pays off. Often it doesn't. And operators absorb the risk either way.

The emissions dependency problem

When a DePIN network has no paying customers, operator rewards come from one place: token emissions. That's fine during a bull market. It's a problem during everything else.

Emissions-funded rewards mean your return is a function of token price, not network revenue. You're not earning from infrastructure services, you're earning from monetary policy. The distinction matters. One is an operating business. The other is a subsidy program with an expiration date.

This isn't a criticism of every supply-first network. Some markets genuinely require coverage before any buyer will commit. You can't sell a connectivity network with twelve nodes. But operators should be clear-eyed about where they sit on the supply-demand timeline and what's actually generating their yield.

A market that didn't need to be invented

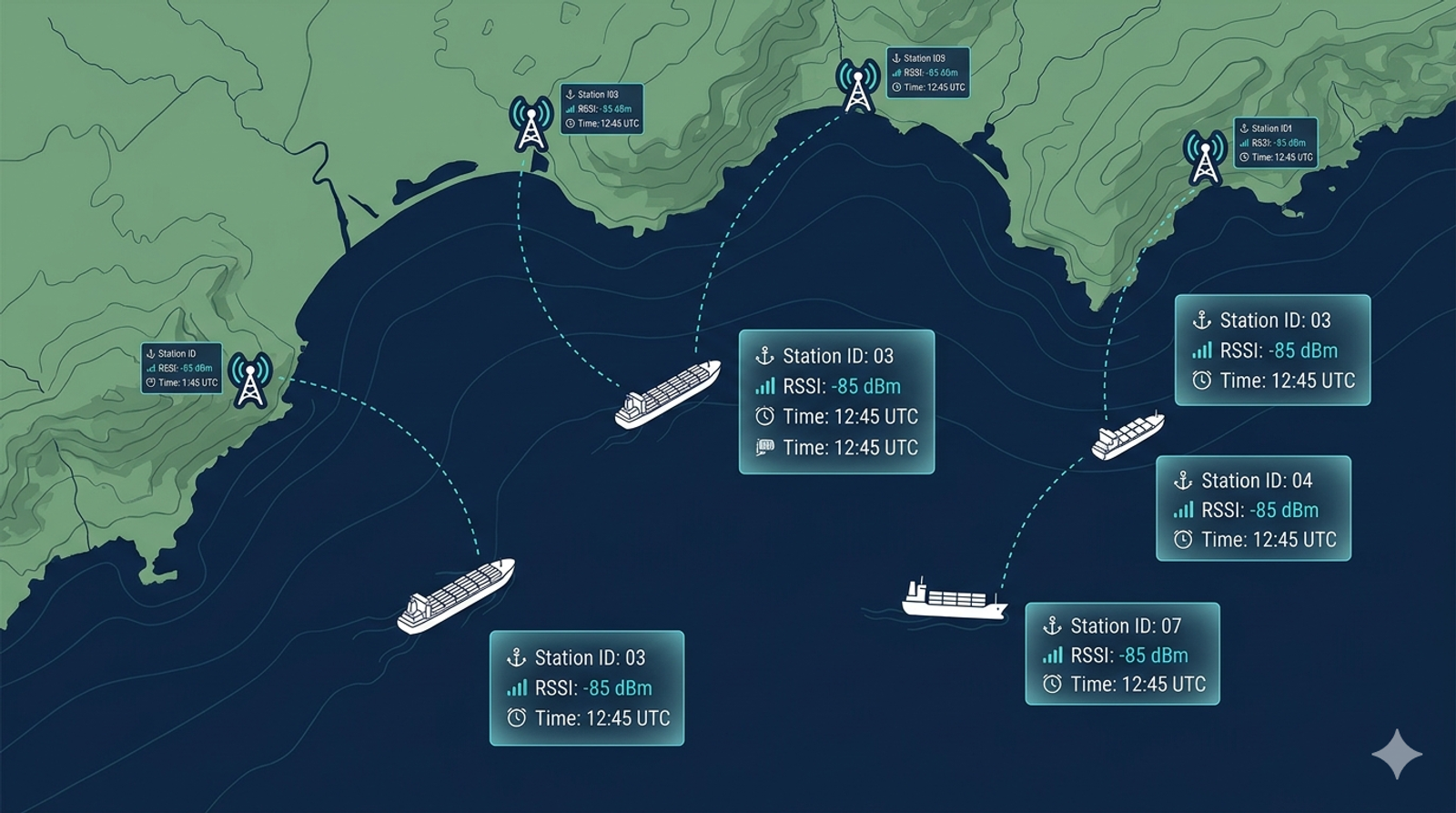

Maritime AIS data is a $2B+ market. It has been for years.

Commodity trading desks pay for vessel tracking to front-run cargo flows. Insurers use it to price hull and cargo risk. Sanctions compliance teams monitor ship-to-ship transfers. Shipping companies optimize fleet routing. AI/ML platforms train models on movement patterns. These aren't speculative use cases on a roadmap. These are budget line items at firms like Trafigura, Glencore, and Lloyd's.

The incumbents serving this market — Kpler, MarineTraffic, Spire — are centralized data aggregators. They operate proprietary receiver networks or buy satellite feeds, package the data, and sell subscriptions. The model works. It has worked for decades. The buyers are real, recurring, and not particularly price-sensitive.

This is the market MastChain entered. Not a market it's trying to create.

What demand-side pull actually changes

When paying customers exist before the network reaches scale, the economics shift in a few specific ways:

Node deployment serves known demand. Coverage gaps map to buyer requirements, not speculative future markets. If commodity traders need better coverage in the Strait of Malacca, a station there serves an identified customer need.

Revenue diversifies the reward structure. Emissions can decline over time without collapsing operator returns, because data sales provide a revenue floor. This is how infrastructure businesses are supposed to work.

Network growth is self-reinforcing. More stations improve data quality through consensus validation. Higher-quality data commands better pricing from enterprise buyers. Better pricing funds better operator economics. The flywheel has a revenue engine, not just a token engine.

Having established buyers doesn't make every station immediately profitable. Placement matters, a coastal station covering a major shipping lane generates more valuable data than one in a landlocked region. Network density matters, confidence scoring requires multiple stations observing the same vessels. Scale matters, enterprise contracts have coverage requirements that a 200-station network serves differently than a 2,000-station one.

The demand-side risk is structurally lower than in most DePIN networks. The execution risk is still real. But if you're evaluating DePIN opportunities based on which networks have actual revenue, not projected revenue, not "partnerships," not roadmap items, the list is short. Maritime AIS data belongs on it because the buyers were never the question.

The infrastructure to serve them was.